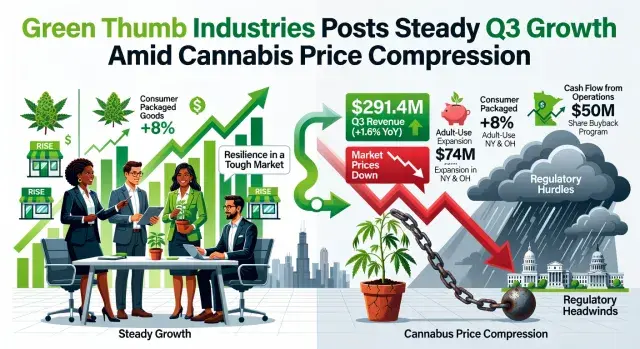

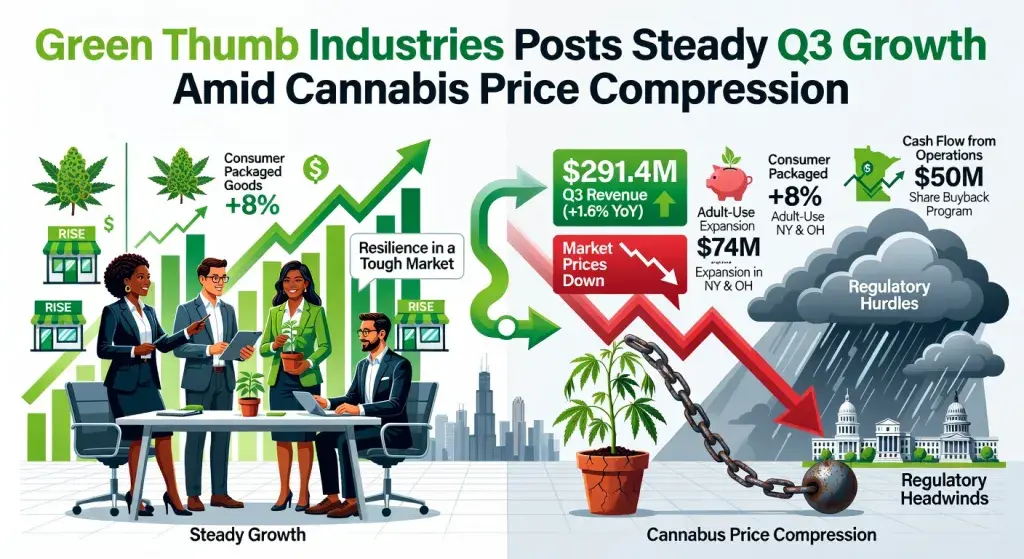

Green Thumb Industries, one of the largest cannabis operators in the United States, reported $291.4 million in third-quarter revenue - a modest 1.6% year-over-year increase that nonetheless signals resilience in a market defined by falling prices and regulatory headwinds. The Chicago-headquartered company, which owns the RISE Dispensary chain, also announced a fresh $50 million share buyback program and flagged its expansion into Minnesota's adult-use market as a growth catalyst heading into 2026.

The Numbers Behind the Quarter

Let's start with what's working. Consumer packaged goods revenue, net of intersegment eliminations, climbed 8%, driven largely by adult-use expansion in New York and Ohio. Cash flow from operations hit $74.1 million - a figure that gives the company significant breathing room. And the balance sheet looks sturdy: $226.2 million in cash against $247.4 million in total debt, with the senior credit facility not maturing for another four years.

Here's the catch. Retail revenue slipped 1%, dragged down by price compression in Illinois, Pennsylvania, and New Jersey - three of Green Thumb's most important states. Comparable-store sales, measuring locations open at least 12 months, fell 7.1% year over year. Gross margin contracted from 51.4% to 49.4%. These aren't alarming declines, but they reflect a structural reality: as more states legalize and more operators enter, wholesale and retail pricing erodes. That pressure isn't going away.

GAAP net income came in at $23.3 million, or $0.10 per share. Strip out the one-time gain from selling intellectual property rights to RYTHM Inc. - a transaction completed in August - and that number drops to $9.7 million, or $0.04 per share. The same figure as a year ago. Adjusted EBITDA was $80.2 million, representing 27.5% of revenue, down from 31.1% in Q3 2024. Profitable, yes. But the margin trajectory is worth watching.

Minnesota Opens, With Caveats

Green Thumb launched adult-use cannabis sales at seven of its eight Minnesota RISE Dispensaries on September 17, 2025, with the eighth following on October 21. The company's President, Anthony Georgiadis, described demand as "strong" but was blunt about regulatory constraints: the current framework in Minnesota, he said, "artificially limits supply and negatively impacts consumers." That's a polite way of saying the state's rollout has been bumpy - supply caps and licensing bottlenecks have constrained what operators can actually put on shelves.

Still, Minnesota represents genuine upside. It's a new adult-use state with meaningful population density, and Green Thumb has eight retail locations already operational. If regulators loosen supply restrictions - a big if - the revenue contribution could be material.

Capital Returns and the Federal Question

Since September 2023, Green Thumb has repurchased roughly 13.5 million subordinate voting shares at an average price of $7.95 per share, totaling about $107 million. The new $50 million authorization extends through September 2026. For a cannabis company, this level of capital return is unusual. Most operators are still burning cash or scrambling for financing. Green Thumb's ability to buy back stock signals something about its operating model that separates it from peers.

CEO Ben Kovler acknowledged the persistent weight of Section 280E - the federal tax provision that prevents cannabis companies from deducting ordinary business expenses - and limited access to traditional capital markets. Federal reform, he conceded, "remains uncertain." But he also pointed to election results in Virginia as an encouraging signal for adult-use legalization there, potentially in 2026.

The company expects fourth-quarter revenue to be "sequentially flat to up single digits." Not a bold projection, but an honest one. In an industry prone to overpromotion, that kind of restraint is worth something.

What This Means for the Broader Cannabis Sector

Green Thumb's Q3 results are a useful barometer for the U.S. cannabis industry writ large. The good news: consumer demand keeps rising. Cannabis is, as Kovler noted, one of the fastest-growing consumer categories in the country. The bad news: growth is being offset by commoditization. Prices fall, margins compress, and operators need scale and brand strength to hold their position.

Green Thumb's strategy - strong balance sheet, share repurchases, selective market entry, and now the RYTHM Inc. transaction enabling THC product distribution beyond dispensary walls - reflects a company preparing for a market that looks more like traditional consumer packaged goods. Whether the federal environment evolves fast enough to reward that positioning is the open question nobody can answer yet.