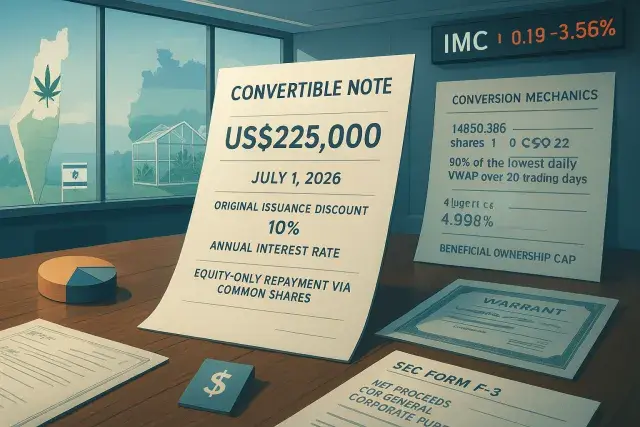

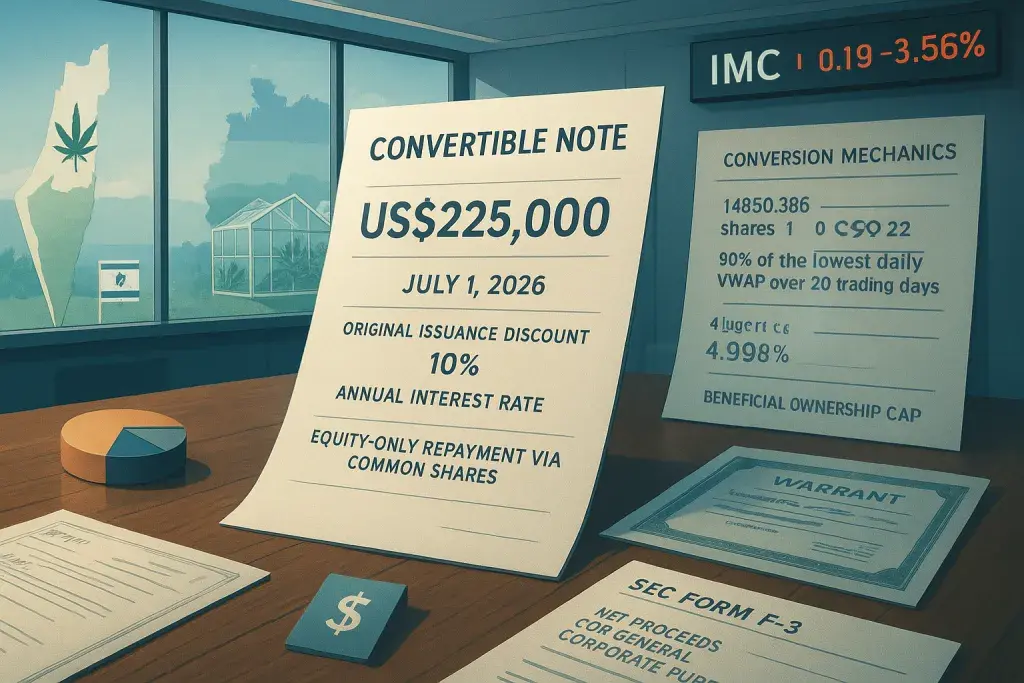

IM Cannabis Corp. has closed a US$225,000 convertible note financing through a private placement with an institutional lender, the company announced July 1, 2026. The deal, structured as a note with a 10% original issuance discount and an 8% annual interest rate, is notable for one specific constraint: it is not repayable in cash. The company's obligations will be satisfied exclusively through the issuance of common shares - a structure that places the full repayment burden on equity dilution rather than operating cash flow.

For a NASDAQ-listed medical cannabis operator with active operations in Israel and Germany, the mechanics of this deal reveal how tight the capital environment remains for internationally focused cannabis companies. Unlike dispensary operators in regulated North American markets who contend with issues like cannabis pos minnesota infrastructure or state-level compliance overhead, companies like IMC face a different kind of operational pressure - one rooted in global capital market skepticism toward cannabis equities, constrained institutional lending appetite, and the structural costs of maintaining licensed operations across multiple regulatory jurisdictions simultaneously.

The conversion mechanics in the July Note deserve close attention. The conversion price is set to the lower of a fixed US$0.152 per share or 90% of the lowest daily volume-weighted average price during the 20 consecutive trading days before conversion - subject to a floor of US$0.0303. That sliding-scale formula, tied to a trailing low rather than a trailing average, is structurally favorable to the lender. In a thinly traded or declining stock, the lender converts at a material discount to already-depressed prices. The floor at roughly three cents per share offers the company some protection against runaway dilution, but the spread between US$0.152 and US$0.0303 is wide - and that range tells you something about where the parties assessed downside risk.

What the Warrant Structure Adds to the Picture

Alongside the note, IMC issued warrants to purchase up to 1,483,386 common shares at C$0.22 per share. The warrants became exercisable immediately on July 1, 2026, and carry a five-year expiration. That's a relatively long runway for the lender to hold optionality on the stock. If the company's equity recovers meaningfully over the next several years - plausible, given potential developments in the Israeli or German medical cannabis markets - the warrant position could prove more valuable than the note itself. For the company, issuing warrants on top of a convertible note is a standard feature of small-cap cannabis financing. It's also a clear signal that the base terms of the note alone weren't sufficient to attract institutional capital without additional upside.

Dilution Risk and the Equity-Only Repayment Model

The no-cash-repayment structure is worth examining carefully. On paper, it removes near-term liquidity pressure - the company doesn't need to generate operating cash to service the debt. In practice, though, converting a note exclusively through share issuance means existing shareholders absorb the cost of repayment through dilution. The 4.99% beneficial ownership cap on the lender limits how aggressively conversion can happen at any one moment, but it doesn't eliminate the cumulative dilutive effect over time. IMC has also committed to reserving sufficient common shares for both conversion and warrant exercise, and to filing a resale registration statement on Form F-3 with the SEC within agreed timeframes - obligations that add administrative and legal cost to what is, at its core, a relatively modest principal amount.

Reading the Broader Signal for Cannabis Business Finance

US$225,000 is a small figure for a publicly listed company. The structure of this deal - deep discount, variable conversion price, equity-only repayment, attached warrants - reflects the reality that institutional lenders to cannabis companies at this market cap level are pricing for significant risk. That's not a criticism of IMC specifically; it's a description of where cannabis capital markets sit for smaller operators and internationally structured companies in mid-2026. Federal prohibition in the United States continues to suppress conventional banking access for cannabis-adjacent businesses, and international operators face an additional layer of complexity: currency exposure, multi-jurisdictional compliance costs, and investor uncertainty about regulatory outcomes in markets like Germany, where adult-use frameworks are still developing. The net proceeds here are designated for general corporate purposes - a broad mandate that gives the company flexibility but offers investors little visibility into how the capital will be deployed. That opacity, combined with the dilutive repayment structure, is the kind of detail that sophisticated cannabis equity investors will weigh carefully.